Amazon Lending: Is It Worth It for Amazon Sellers?

The Amazon Lending program offers business loans for registered Amazon sellers, but are the costs worth it? Is it a good choice for your Amazon business?By ITJuly 31, 2018

Since its origin in 2011, Amazon Lending has surpassed $3B in loans to over 20,000 businesses on Amazon. Additionally, over 50 percent of the companies have eventually taken a second loan from the e-commerce powerhouse.

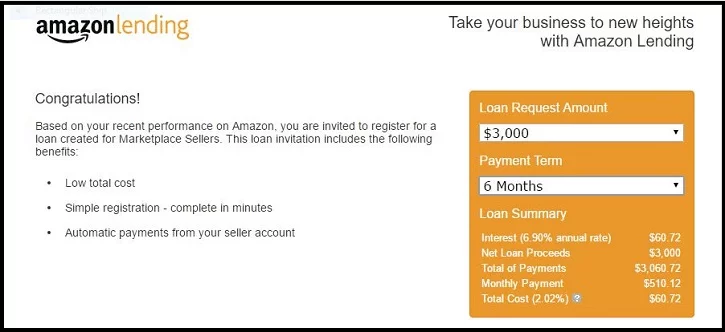

An invitation-only program, Amazon Lending invites established sellers and brands to participate in the program for the sole purpose of purchasing more inventory to sell on the marketplace. Amazon prequalifies you based on your sales volume and other data metrics. Borrowers are invited to apply after various durations of time selling on the marketplace — there’s no specific amount of time that you need to be selling for to qualify. The email invitation to join will come from Seller Central or right to your email inbox and will look something like the notification pictured below.

The Amazon Lending program offers its merchants loans that range from $1,000 to $750,000.

Amazon Lending Requirements

The Amazon Lending program offers its merchants loans that range from $1,000 to $750,000. As seen above, the Amazon Lending invitation contains a loan offer up to a certain amount, as well as a range of repayment terms to choose from. You have the opportunity to accept all or part of the offered amount and can choose your terms. The calculator figures your interest based on the terms you choose, so you will know exactly what the loan will cost you. Amazon then deposits funds into your bank account, typically within one or two days, which you can then use to accelerate your inventory position on Amazon.

For eligibility in the program, Amazon references your sales history, inventory position and maintenance, and customer service performance metrics. If your Amazon sales don’t cover the automatic payment, Amazon will deduct the outstanding amount via ACH from your bank account and if you can’t pay back the loan according to its terms, Amazon has the ability to take your FBA inventory and sell it to themselves to settle any remaining debt.

Interest Rates and Loan Terms

Geared to short-term funding, Amazon Lending payment terms are twelve months or less. Although Amazon has not disclosed the rates on its loans, it has told Bloomberg that interest rates on its loans are lower than those of credit cards and merchant cash advances. For business credit cards, annual percentage rates are typically 12% to 22%, while merchant cash advances range from 40% to 350%.

It is important to note that the APR differs from the interest rate, as the annual percentage rate can include other fees and determines the yearly cost of the loan. Like a merchant cash advance, Amazon takes a fixed percentage of gross sales from your seller account each month until the loan is repaid, regardless of your sales performance on the marketplace. Amazon has partnered up with Bank of America Merrill Lynch in order to mitigate risk and access capital for the specific intent of providing credit to more merchants for inventory, but additional information is unavailable as the partnership details are confidential.

Stay on top of the latest e-commerce and marketplace trends.

Amazon Lending Pros and Cons

After you have been invited, there are several benefits that make accepting the loan from Amazon a smart decision for your business.

1. Smooth application process. When applying for business financing, you typically have to compile several business loan requirements, such as credit reports, bank statements, a balance sheet, profit and loss statements, and tax returns, to name a few. Gathering all of this sensitive information is a timely and meticulous process. With Amazon Lending, you can accept, decline, or request changes to the loan directly on the invitation’s portal. The program does not require information such as your credit score, tax returns, time selling, or financial profile. As a seller, Amazon already has your sales history and personal information so the funding process is fast and convenient.

2. Lower interest rates and high borrowing amounts. With short-term loans and merchant cash advances, borrowers can face tremendously high interest rates. With Amazon Lending, the maximum interest rate you can expect will likely be around 16% on a loan with a twelve-month term. Additionally, you can borrow up to $750,000 — an amount that can make a significant impact on your inventory optimization process. However, the maximum borrowing amount is based on your sales performance, so you will need strong conversion rates to land higher borrowing amounts.

3. Fewer fees. With financing, borrowers tend to face a slew of fees with their loan such as origination fees, application fees, closing fees, prepayment penalty fees, and more. With Amazon Lending, there are no origination fees or prepayment penalty fees, which are the ones that lenders collect if you pay off your loan early. If you pay your Amazon Lending amount back early, you will save on your loan in the long run.

There are also some disadvantages to consider prior to jumping into the Amazon Lending program right away. It’s important to remember that Amazon business are not one size fits all, so you should weigh your options and pick the financing route that makes the most sense for your business goals.

1. Limited use of funds. Amazon is extremely specific as to what their loans can be used for — inventory optimization. The loans can not be used to fine-tune any other aspect of your business except for building up or restocking inventory of your marketplace items.

2. Fixed deductions from your Amazon seller account. Amazon charges you for each sale you make on their marketplace via the referral fee. If you move forward with a loan from Amazon, the company will automatically deduct a fixed monthly amount from your Amazon seller account, regardless of sales, until your loan is repaid.

3. Your inventory may be at risk. If you default on your loan, Amazon has the right to claim your inventory in order to recoup the costs that they lose on the loan. If you are an FBA seller, Amazon can hold your inventory as collateral until you pay them back or seize your inventory as their own and sell it to get their money back. If you utilize a merchant fulfilled model and default on your loan, your ongoing sales proceeds on the marketplace will go right to Amazon as repayment of your loan, instead of to your seller account.

4. High monthly payments. Due to the fact that Amazon’s repayment terms are shorter than regular business loans and usually cap at twelve months, your monthly payments could be higher than what is sustainable for your business depending on your all-in borrowed amount.

About the Author

Should You Use an Amazon Loan for Your Business?

Whether you are expanding your Amazon business internationally, pursuing a new market domestically, adding a new product category to your assortment, or preparing for a new season or holiday, financing your business venture and having the capital to take that next step can sometimes pose an issue for sellers and brands. If a large portion or all of your business goes through Amazon and having a stronger, more controlled handle on inventory would help solve an ongoing business issue, Amazon Lending might make sense for you to pursue upon being invited. Knowing your flexibility and what your business is trying to accomplish with the loan will significantly aid your decision process if you have been invited to participate.

![Preparing for Q4: Why Reputation Matters [Webinar Recap]](https://feedvisor.com/wp-content/uploads/2018/07/blog-preparing-for-q4-why-reputation-matters-280x280.jpg.webp)